The rise of the Software Defined Vehicle

Welcome to accilium‘s new series „The rise of the Software Defined Vehicle in the automotive industry“. Here we explore the biggest challenges of traditional OEMs and suppliers and how the transformation towards SDV enablement can be achieved.

The automotive industry stands at the cliff of a profound transformation, driven by the newest technology and evolving customer demands. At the forefront of this paradigm shift are software-defined vehicles (SDVs), indicating a new era in automotive innovation and functionality.

As the automotive landscape evolves, new requirements and trends emerge and challenge traditional business models and practices. From the growing emphasis on connectivity and autonomous driving to the demand for personalized entertainment experiences, these shifts are turning the industry and its corresponding activities upside down.

We will provide insights from our daily work and share our key takeaways for successfully moving into a new era of vehicle development. Therefore, we will delve into six deep dives over the upcoming 6 weeks to dig deeper and to illustrate our point of view:

- Corporate strategy: New orientation of companies to ensure future competitiveness.

- Business model & customer: Adaptions to value streams to fulfill changing customer demands.

- Organization: Re-structuring to enable the organization to realize new requirements.

- Product development & technology: Adoption of innovative approaches to reduce complexity while fulfilling demands.

- Process, methods & tools: Changes to the workbench to ensure effectivity and efficiency of product development.

- Supplier & partnering: Challenge of supplier relationships to guarantee the company’s ability to deliver.

1. Corporate strategy: New orientation of companies to ensure future competitiveness.

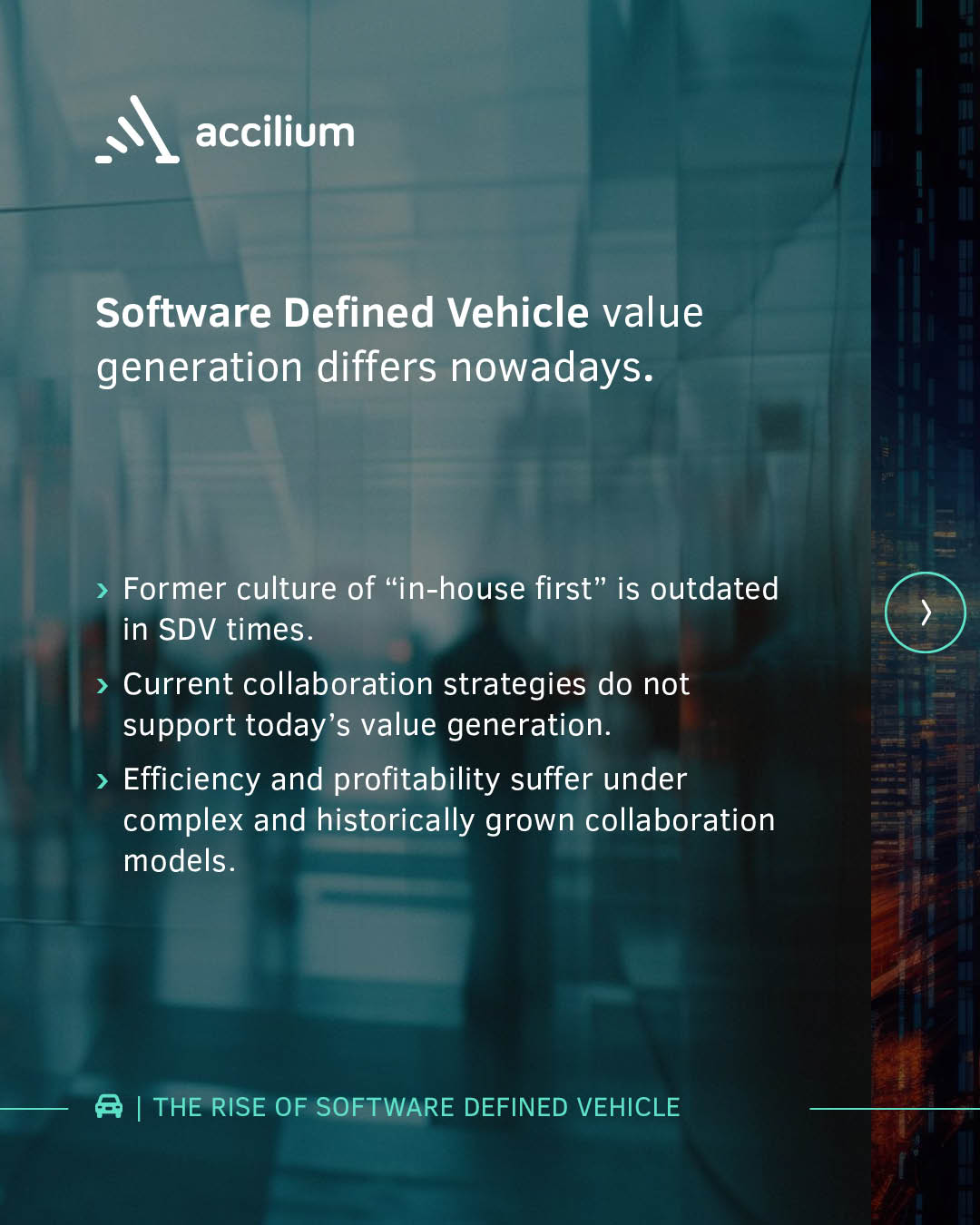

Traditional collaboration strategies of many companies have often evolved over time. Nowadays they are facing new challenges due to the shift in value creation towards software. This can result in financial risks for companies if customer requirements cannot be realized or in-house development is not profitable in the long term.

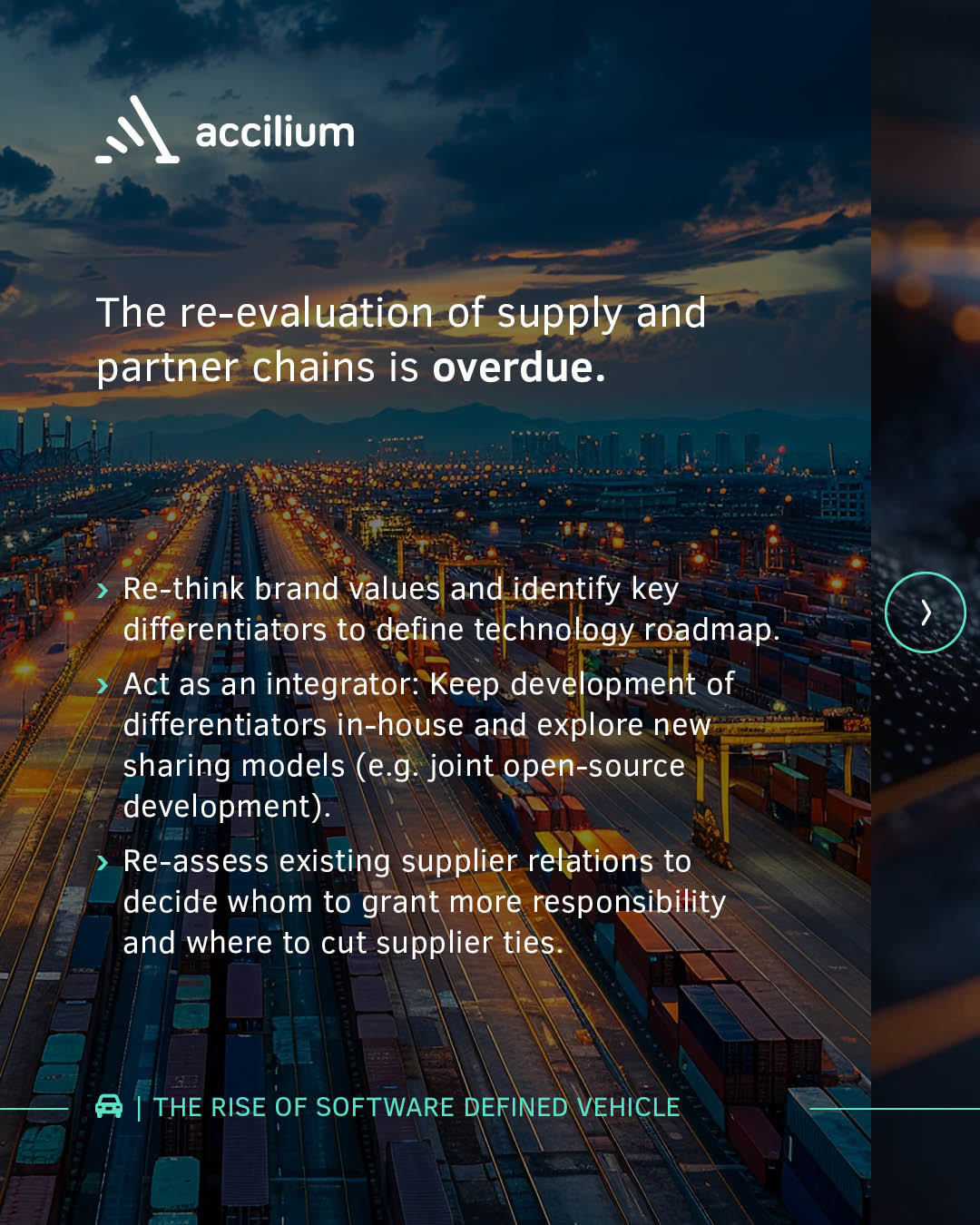

In order to remain competitive, companies must set apart themselves with clear differentiators and reflect this in their technical roadmaps. The future role of OEMs (original equipment manufacturers) is therefore evolving towards “integrators”. They are handing over more responsibilities to suppliers and partner such as Tier 0.5s and opening up to share models in addition to the classic make or buy strategies, such as open-source development.

A well-founded strategic positioning is crucial for the determination regarding make, buy or share. These decisions are then implemented by the relevant sub-organizations, particularly in development and purchasing.

2. Business model & customer: Adaptions to value streams to fulfill changing customer demands.

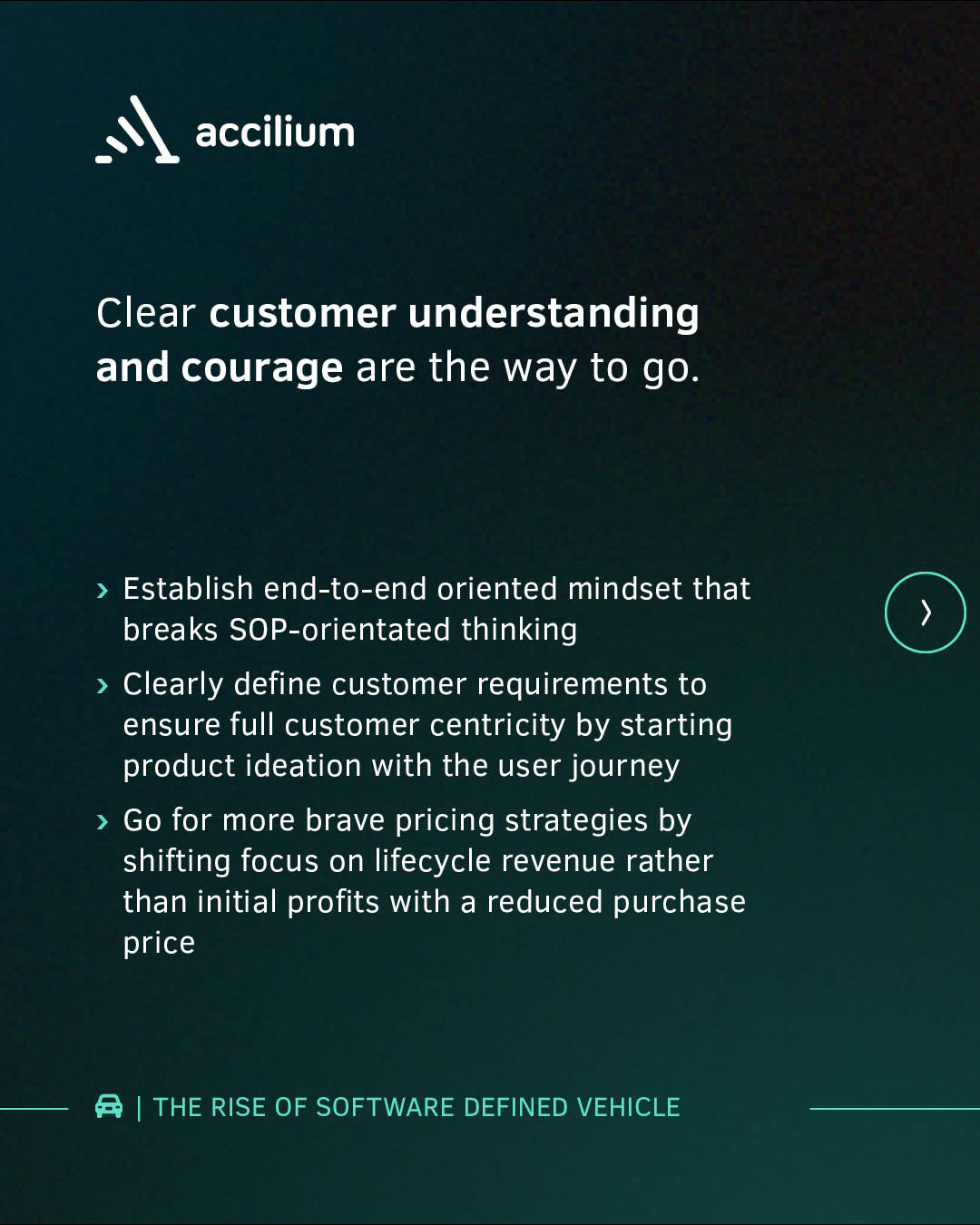

As software integration in cars accelerates, traditional value and monetization models are outdated and therefore evolving. The evolving presence of software features and the difference in product and development cycles of software and hardware are unlocking exciting new opportunities for in-car monetization. To remain competitive, it’s essential to seize these new opportunities and adapt to the changing landscape of customer experience.

Adopting a holistic, end-to-end customer experience mindset, and moving away from outdated SOP (start of production) thinking, is crucial. By focusing on lifecycle revenue generation rather than immediate profits, the foundation is set for future competitiveness. Strategic pricing and marketing initiatives will be key catalysts in this transformation.

In close cooperation, development and production are responsible to firstly enable in-car monetisation by then showing the ability to align release methods and cycles with mechanical car development and customer needs.

3. Organization: Re-structuring to enable the organization to realize new requirements.

In the future, E/E architectures will play a pivotal role in delivering cutting-edge customer features. Current architecture generations are reaching their limits but are pivotal for managing and reducing the complexity of vehicles. Additionally future-proof E/E architectures are designed to support in-car software updates for the next fifteen years, ensuring vehicles stays at the forefront of technology.

With E/E architectures built around a central computer supported by a zonal structure, they can provide maximum flexibility and adaptability. This innovative design allows for seamless changes and upgrades throughout the vehicle’s lifetime. With architects maintaining a strong role and mandate, a structured and sustainable approach to E/E platform design can be assured.

To achieve these groundbreaking advancements, one must start fresh: Moving away from outdated brownfield methods and beginning from scratch is the most technologically sustainable path forward. Corporate support is essential, recognizing the immense savings from avoiding retrofitting and unlocking untapped future customer features.

Get in touch with us:

Johannes Florian

Associate Partner

Michael Weingärtner

Associate Partner