Synthetic fuels, known as E-fuels, are increasingly becoming a focal point in global decarbonization efforts. They are produced using electricity from renewable sources, water, and captured carbon dioxide (CO2). E-fuels represent a promising option, particularly for sectors where electrification is challenging, such as aviation, shipping, and heavy-duty road transport. Despite their potential, E-fuels face significant hurdles regarding cost, production scale, and the necessary infrastructure. The following sections examine the role of E-fuels, current challenges, and measures required for their broader adoption.

The Need for E-fuels in the Transport Sector

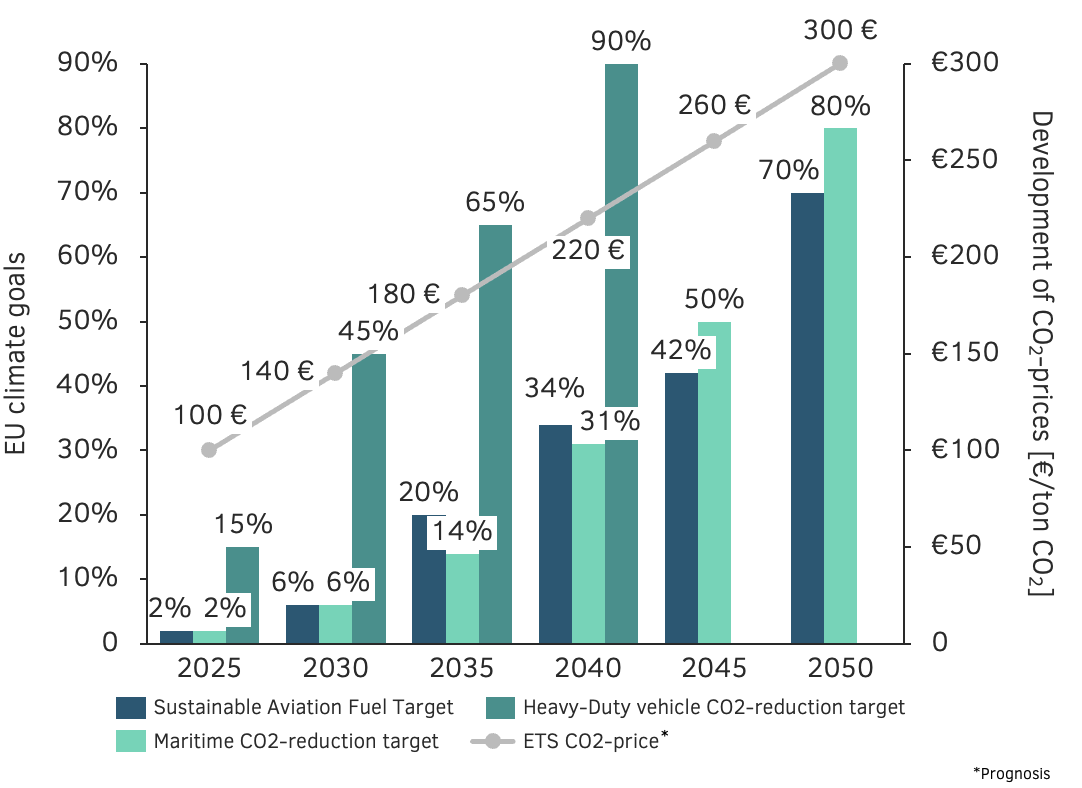

The transport sector is a major emitter of greenhouse gases. Globally, road transport accounts for approximately 15% of CO2 equivalent emissions, aviation for about 3%, and shipping for around 2%.¹ Drastic emission reductions are essential to achieve climate targets. The European Union, for instance, aims for a 55% reduction in emissions by 2030 and climate neutrality by 2050 under its “Fit for 55” package. Specific targets for transport include a 90% emissions reduction for new heavy-duty vehicles by 2040 and ambitious blending quotas for sustainable aviation fuels (SAF), rising to 70% by 2050. Maritime shipping is also targeted to reduce greenhouse gas intensity by 80% by 2050.² E-fuels offer a pathway to support these objectives.

Potential and Challenges of E-fuels

The primary potential of E-fuels lies in their ability to significantly reduce emissions. Sustainable aviation fuels (SAF), which include E-kerosene, can cut CO2 emissions by up to 80% compared to fossil kerosene. Another advantage is the potential to continue using existing fueling and propulsion infrastructure, which could ease the transition.

However, considerable challenges remain. The cost of E-fuels is currently high. Projections suggest they could be four times more expensive per kilometer than battery-electric vehicles by 2030 and two to eight times more expensive than fossil alternatives. Production costs are around €50 per liter and need to decrease substantially. Production volume is also still low. Global SAF production reached one million tonnes in 2024, merely 0.1% of global jet fuel consumption. For significant market penetration, 3,000 to 6,500 new production plants would be needed globally. The required infrastructure for renewable electricity (estimated at 2,000 TWh by 2030), electrolyzers, CO2 capture, and bunkering demands massive investments, for example, $10-30 billion for port infrastructure for shipping alone.3

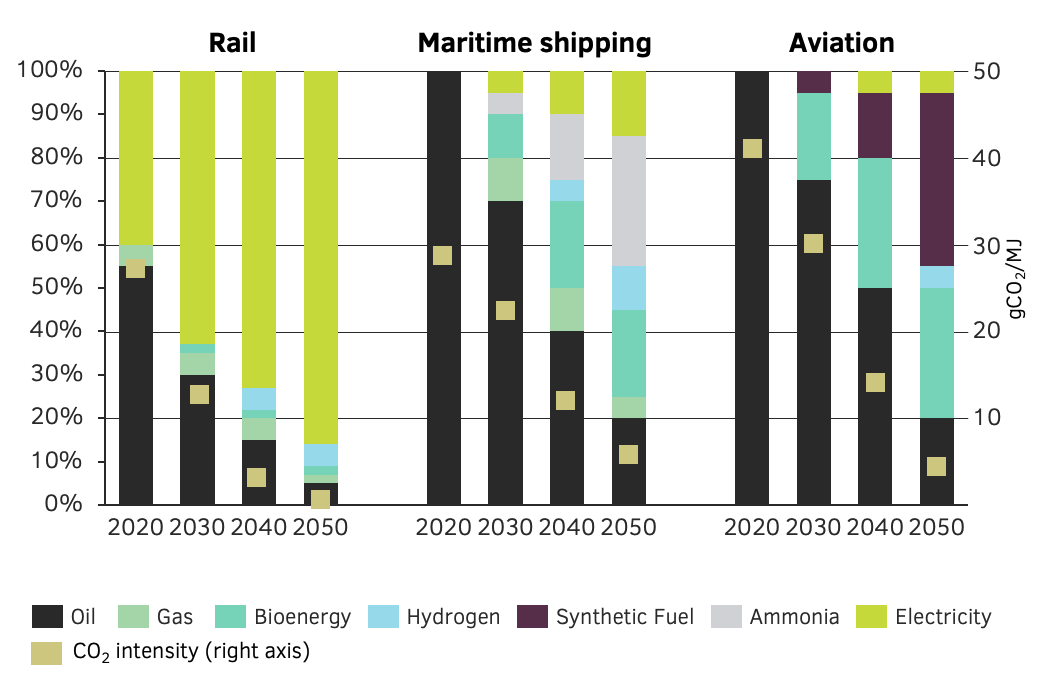

Different types of E-fuels, such as E-methanol, E-ammonia, and E-LNG (synthetic liquefied natural gas), have specific pros and cons regarding energy density, safety, and cost. E-methanol is already in use but is 3-5 times more expensive than fossil fuels. E-ammonia has high CO2 reduction potential but is toxic and requires stringent safety standards. E-LNG is most similar to fossil LNG but still produces CO2 emissions and faces issues with methane slip.

Policy Frameworks and Market Development

Policy mandates are a crucial driver for E-fuel development. EU regulations like “Fit for 55,” ReFuelEU Aviation, and FuelEU Maritime create demand certainty and incentivize investment.² Germany’s technology-neutral stance, allowing E-fuel-powered vehicles beyond 2035, supports this trend. Airlines are already signing long-term offtake agreements for SAF, enhancing investment security. E-fuels are expected to initially establish themselves in niche segments where battery-electric solutions face limitations, such as in heavy-duty transport, aviation, and maritime shipping.

Strategies for Successful Scaling

Concerted efforts are necessary to successfully establish E-fuels.

These include:

Investments: Public funding and guaranteed offtake contracts are important to stimulate private investment and mitigate risks.

Technology and Innovation: Further development of Power-to-Liquid processes and production efficiency improvements are critical for cost reduction.

Infrastructure Development: Coordinated expansion of renewable energy sources, electrolysis capacity, CO2 capture facilities, and distribution and bunkering infrastructure is required.

Policy Support: Continued strong mandates, subsidies, and effective carbon pricing are necessary to improve competitiveness.

Conclusion: The Role of E-fuels in a Sustainable Transport Future

E-fuels are an important component in achieving net-zero targets, especially in hard-to-decarbonize transport sectors. Overcoming hurdles related to cost, production scale, and infrastructure is paramount. Close collaboration between policymakers, industry, and research is essential to unlock the potential of E-fuels. Together with other climate-friendly technologies, they can pave the way for a more sustainable transport system.

Looking for deeper insights?

1Statista, World Emissions Clock

2ReFuelEU Aviation/FuelEU Maritime

3 IEA Net Zero by 2050

ISO/IEC 27001:2013 certified

ISO/IEC 27001:2013 certified